Stop trying to do tech-based economic development without the Department of Defense

The standard playbook isn't working. The rest ain't rising. Here's a better way.

New ventures rooted in regional economies without large venture capital firms – and that’s all of us outside of the Bay Area, Boston, New York, and perhaps a handful of other cities – struggle to raise private financing necessary to build and validate a product. The “Valley of Death” is more than just an inconvenience for tech startups; it’s a fundamental defect in the American model and it threatens our national security. At every step in the technology development process, the Department of Defense is mobilizing financing programs to bridge this gap.

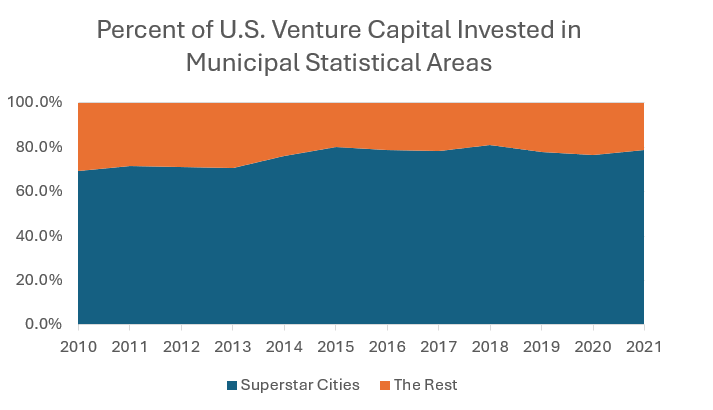

Are venture capital firms stubbornly refusing to locate and invest outside of the Bay Area and the other superstar cities and missing out on value creation elsewhere, as many advocates for non-superstar insist? Or are venture capital firms simply choosing to locate where value is being created?

It’s the latter, according to a 2010 paper by Harvard Business School’s Josh Lerner, looking at fund performance and geographic location of more than 1,000 venture capital firms.

“(V)enture capital offices are concentrated in locales where previous investments by venture capital firms were successful,” Lerner wrote, adding that “moving from the 25th percentile of the regional success rate for venture capital investments over the past five years to the 75th percentile of the regional success rate increases the number of offices in a (Combined Statistical Area) by a factor 2.3.”

Put simply, according to Lerner, first startup communities must demonstrate they can create value, then comes VC – not the other way around.

As venture capital funds raised dramatically more capital during the low-interest rate environment of the 2010s, it’s possible that countervailing evidence of Lerner’s thesis has emerged. But I haven’t seen a shred of evidence that civic efforts to attract VC into non-superstar cities have fundamentally changed the economic and business dynamics that have agglomerated so much venture activity in the superstar cities.

I believe the evidence is clear. Venture capital is not elevating non-superstar cities to economic parity. Regional economic leaders need to fundamentally rethink the standard venture community model that directs startups to pitch businesses in front of investors who are often unwilling or unable to support high-risk technologies.

Regional economies outside of the superstar cities should instead focus attention on more patient sources of capital and federal funding programs designed to advance high-risk technologies through small businesses. Federal dollars – especially a new suite of national security-focused funding sources – can and should serve as a bridge to later private capital financing.

In this commentary, I will explain how regional economies can reorient venture communities toward more effective early-stage financing pathways, specifically those that lead into prime defense contractors and the doors of the Pentagon. As I have explained previously, defense tech is tech and any regional economy that would like to call itself a superstar should aspire to more deeply engage the national security community.

National strategic challenge

The sustainability of defense tech ventures has become an urgent national security matter, and Washington lawmakers have only recently begun equipping the Pentagon with the tools to protect critical vendors.

After World War II through the end of the Cold War, the Pentagon’s search for technologies didn’t need to go any further than the large defense contractors. Multi-national defense companies were an essential element not only of America’s defense industrial base, but of the entire American innovation engine. They spared no expense to hire America’s top engineers in leading technology fields, and commercialized research from defense and university laboratories.

The market changed in 1993 after new Clinton Administration Defense Secretary Les Aspin urged the Pentagon’s 15 largest defense contractors to consolidate ahead of the looming Pentagon budget cuts. By consolidating defense suppliers, Aspin had hoped the industry would gain efficiencies without losing capacity. And on command, a wave of mergers conjoined the Pentagon’s suppliers into five mega-contractors: Lockheed Martin, Boeing, Raytheon, Northrop Grumman, and General Dynamics, collectively called the “big five” in defense circles.

The legacy of Aspin’s directive is a more consolidated defense market that, to many observers, has undermined incentives for supporting R&D. The big five were awarded nearly two-thirds of the Defense Department’s R&D contracts in 2006; by 2015, that number dropped to just 33 percent.

Make no mistake: The big five are far from middlemen. Indeed, the Pentagon has come to rely on the big five to effectively manage the defense technology market, with R&D projects largely done by smaller, alternative suppliers.

The F-35 program tells the story. Lockheed Martin was the prime, but more than 200 subcontractors, some big but many small, provided designs and technologies to ultimately complete the F-35. Small contractors provided essential elements of the F-35 control panel, enabling software, chemical coatings, and a host of other F-35 components.

Take also hypersonic missiles capable of traveling faster than the speed of sound and hitting a target within inches anywhere on the globe. Logically, no startup can design and produce this kind of advanced technology. But smaller elements – such as advanced materials capable of withstanding extreme heat – are the domain of smaller suppliers, selling wares to the primes.

Perhaps it’s no surprise that this prime-sub relationship that forms the framework of the entire national security industry yields a large volume of mergers and acquisitions, which have reached record levels in recent years.

Yet by leaving itself at the whims of the market, the Pentagon is virtually powerless to prevent acquisitions that result in the shutting down of R&D projects by the acquired firm. This often occurs when continuing development of the technology does not align with the acquirer's business interests, regardless of the technology’s national security importance.

The Department of Defense has also learned how sources of capital from adversarial sources, namely China, can strip critical capabilities from its control. Their concerns were most vividly illustrated in 2017 after Neurala, a Boston-based AI company that had been working with the Air Force to develop sensory capabilities for robots. Unable to raise necessary capital in the United States, Neurala could only find capital from a state-backed investment firm in China.

Department of Defense actions

Across the Obama, Trump I, and Biden administrations, the Department of Defense has initiated successive programs to expand the defense industrial base and protect non-traditional vendors. Yet programs in themselves are not enough. The Pentagon has also gained new authorities to streamline acquisitions for nontraditional suppliers and directly provide bridge financing to cross valleys of death. In doing so, the Department of Defense is pushing into new frontiers of American industrial policy, discarding free market absolutism.

In 2016, Congress granted the Pentagon Middle Tier of Acquisition (MTA) authorization, enabling acquisition officials to work with suppliers of technologies considered ready for deployment within five years, using a more streamlined acquisitions process.

The Air Force’s AFWERX introduced its Strategic Funding Increase (STRATFI) program in 2020 to provide an additional layer of funding after the two-phase Small Business Innovation Research (SBIR) program. Firms that had received an SBIR Phase II award, typically around $1 million, receive as much as $15 million in additional support under STRATFI to complete development of a technology.

In 2022, the Department of Defense launched the Office of Strategic Capital (OSC) to act something like a bank, issuing loans and loan guarantees to firms operating in critical technology areas. OSC was provided nearly $1 billion by congressional appropriators in 2023 and issued its first public solicitation last September.

The Defense Innovation Unit pushed Congress to approve a $1 billion “hedge portfolio” in the 2024 National Defense Authorization Act (NDAA) to fund development and field systems within three years that directly address front-line operational challenges.

The Pentagon is now making dramatically more frequent use of Other Transaction Authority (OTA) contracts each year – more than 15,000 OTA contracts since 2016 and more than $15 billion in OTA contracts in 2023 – that provide acquisitions officials greater flexibility in writing terms of awards that typically permitted.

Just two weeks ago the Department of Defense announced its first 18 Small Business Investment Company Critical Technologies Initiative (SBICCT) Licensed and Green Light Approved funds. The Pentagon projects these funds will invest as much as $4 billion into 1,700 companies in 14 critical technology areas. Notably, 11 of these funds will maintain offices in non-superstar markets, including five funds who will operate exclusively outside of the superstar cities.

To state the obvious: These actions, viewed collectively, assert the Department of Defense as a central actor in the American technology economy, whether or not regional economic leaders recognize it as one.

Opportunity for regional economies

As the beginning of this commentary, I noted the clear futility of efforts to attract venture capital into non-superstar cities. This is precisely why non-superstar cities should be so aggressive in building their own defense-tech communities. Department of Defense programs can and are taking on early-stage business and technology risk, leaving value on the table for corporate partners, private equity firms, and regional economies.

Indeed, small defense contractors rarely receive venture financing and instead frequently support initial growth with federal grants and contracts. Without the need to share ownership with venture capital investors, defense tech firms do not need to locate in major VC hubs, namely the Bay Area, Boston, and New York. They can instead commercialize research done closer to home – R&D done at universities and federal laboratories is far more diffuse than the VC market – and engage Department of Defense initiatives put in place to expand the American defense industrial base and find technologies that the Pentagon urgently needs to acquire.

I believe, given the extraordinary scale of activity, regional economies need to build centers to bridge their own regional innovation communities with the Pentagon. The Pacific Northwest Mission Acceleration Center in Seattle and the Defense Alliance in St. Paul, Minnesota, are two such centers. My own organization, the Frontier Mission Network, aims to become a similar center in Chicago.

What functions could these centers provide (perhaps already are)? Specifically, they could:

Build relationships with Department of Defense contracting officers and program managers on behalf of local innovation communities.

Understand and guide small business and new ventures through Federal Acquisition Regulations (FAR) and non-FAR contracting mechanisms.

Monitor and communicate Department of Defense funding programs for non-traditional suppliers and requirements.

Provide a cross-regional platform to facilitate technology licensing for new ventures, then engage experienced R&D professionals to review development plans before seeking licensing agreements from research institutions and submitting funding proposals to the Department of Defense.

Engage corporate and civic stakeholders to support funding proposals with clear roadmaps toward dual-use product development.

The end product of this activity would be investor-ready deal flow. And we’re getting to work to provide it:

Next challenge: By definition, “dual-use” technologies operate at the intersection of national security and commercial challenges. An urgently pressing example is the need to safeguard economic choke points – whether satellites or trade routes – where adversaries are attempting to disrupt the flow of critical information and goods.